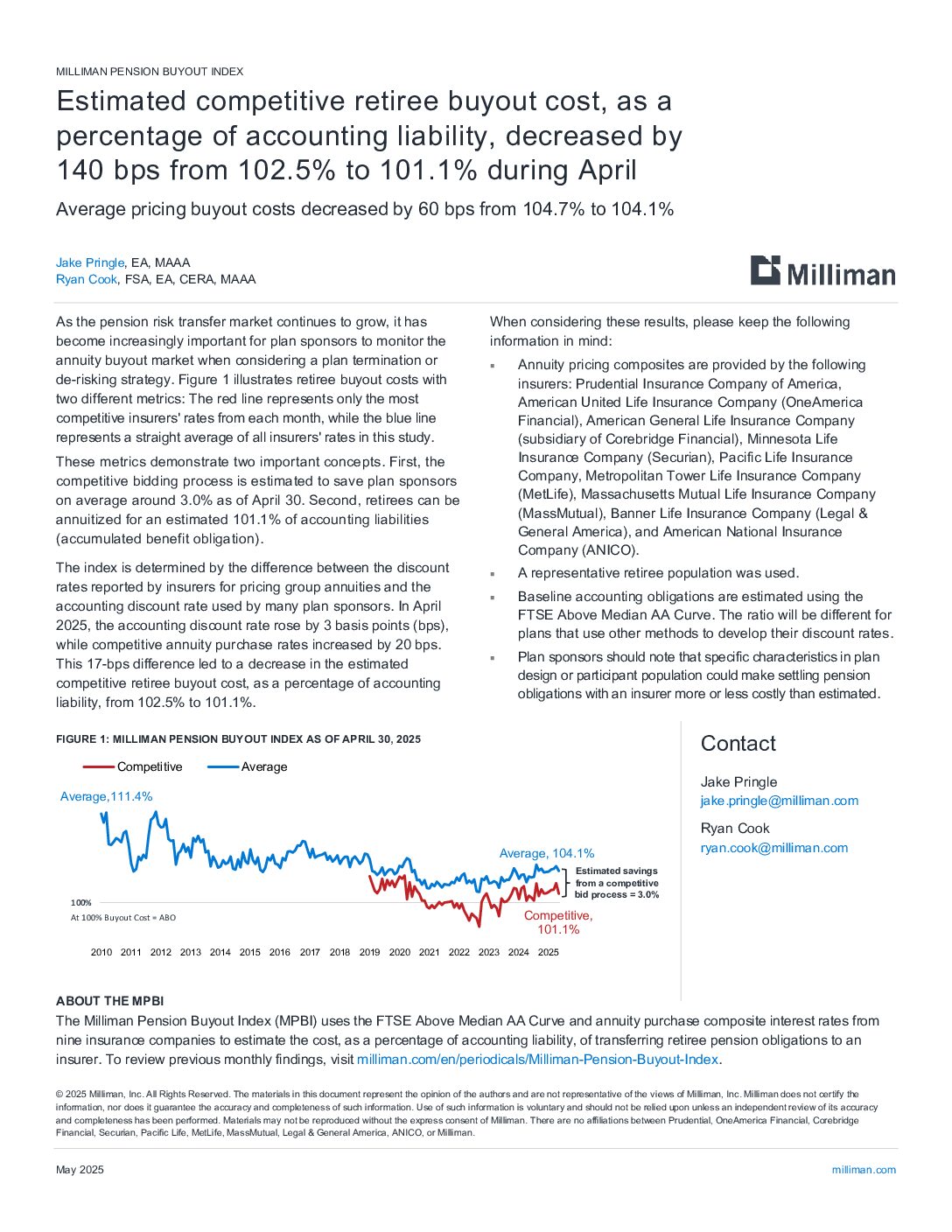

Milliman Pension Buyout Index May 2025

By Jake Pringle & Ryan Cook Estimated competitive retiree buyout cost, as a percentage of accounting liability, decreased by 140 bps from 102.5% to 101.1% during April As the pension risk transfer market continues to grow, it has become increasingly important for plan sponsors to monitor the annuity buyout market when considering a plan termination or de-risking strategy. Figure 1 illustrates retiree buyout costs with two different metrics: The red line represents only the most competitive insurers' rates from each month,...